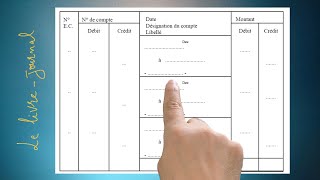

What Is a Livre De Comptes?

The term Livre De Comptes (French for “book of accounts”) refers to the systematic record‑keeping tool used to capture every financial transaction of an organization. Whether the entity is a small boutique, a medium‑size enterprise, or a nonprofit, the Livre De Comptes serves as the primary source of truth for cash flow, profitability, and compliance. By documenting debits and credits in a structured format, it enables managers, auditors, and tax authorities to understand the financial health of the business at any moment.

Historical Roots

Early merchants in medieval Europe kept simple handwritten ledgers to track sales and expenses. The practice evolved dramatically after Luca Pacioli published his treatise on double‑entry bookkeeping in 1494, a method that quickly spread across France and the rest of Europe. The French adaptation became known as the Livre De Comptes, standardising the way assets, liabilities, revenues, and expenses were recorded. Over centuries, the book transformed from parchment pages to printed journals and, finally, to digital platforms.

Core Sections of a Traditional Livre De Comptes

- Assets – Cash, inventory, equipment, and any other resources owned by the entity.

- Liabilities – Obligations such as loans, supplier invoices, and accrued expenses.

- Equity – Owner’s capital, retained earnings, and any share‑based contributions.

- Revenue – Sales, service fees, and other income streams.

- Expenses – Costs incurred to generate revenue, including salaries, rent, utilities, and depreciation.

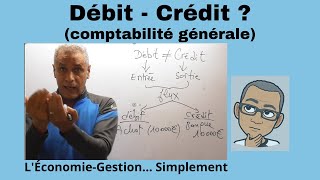

Each entry follows the double‑entry principle: every debit recorded in one section must have a corresponding credit in another, ensuring the accounting equation (Assets = Liabilities + Equity) remains balanced.

Why Maintaining a Livre De Comptes Matters

Accurate bookkeeping delivers several tangible benefits:

- Informed decision‑making – Managers can compare actual performance against budgets, identify trends, and allocate resources more effectively.

- Regulatory compliance – French commercial law and international standards (such as IFRS) require a clear audit trail; the Livre De Comptes satisfies that requirement.

- Financial transparency – Stakeholders, including investors and banks, rely on the book to assess risk and creditworthiness.

- Tax accuracy – Properly recorded revenues and deductible expenses simplify the preparation of tax returns and reduce the risk of penalties.

Transition to Digital Solutions

Modern businesses rarely use paper ledgers. Accounting software replicates the structure of the traditional Livre De Comptes while adding automation, real‑time reporting, and cloud‑based backup. Popular features include:

- Automatic posting of recurring transactions.

- Integration with bank feeds to reconcile accounts daily.

- Generation of financial statements (balance sheet, profit & loss) at the click of a button.

- Role‑based access controls that protect sensitive data.

Despite the technological shift, the underlying principles remain unchanged: every transaction must be recorded with a debit and a corresponding credit, and the ledger must stay balanced.

Best Practices for Keeping a Reliable Livre De Comptes

- Record promptly – Enter transactions as soon as they occur to avoid omissions.

- Use consistent chart of accounts – Standardise account codes and descriptions across the organization.

- Reconcile regularly – Match ledger entries with bank statements, supplier statements, and inventory counts at least monthly.

- Document supporting evidence – Attach invoices, receipts, or contracts to each entry for auditability.

- Review and correct errors – Conduct periodic internal audits to spot and fix imbalances before external auditors arrive.

Common Mistakes to Avoid

Even experienced accountants can slip into habits that compromise the integrity of the Livre De Comptes. Typical pitfalls include mixing personal and business expenses, neglecting accruals at period‑end, and failing to adjust for depreciation. Each of these errors distorts the true financial picture and may trigger regulatory scrutiny.

How the Livre De Comptes Supports Strategic Planning

Beyond compliance, the ledger is a strategic asset. By analysing trends in revenue streams, cost centres, and cash‑flow cycles, executives can forecast growth scenarios, evaluate investment opportunities, and negotiate better terms with suppliers or lenders. The granular data stored in the Livre De Comptes also feeds performance dashboards, enabling real‑time KPI monitoring.

Conclusion

The Livre De Comptes remains the backbone of sound financial management, whether maintained on paper or within a cloud‑based accounting system. Its disciplined approach to recording debits and credits provides clarity, ensures compliance, and empowers decision‑makers with reliable data. By adhering to best practices—prompt recording, regular reconciliation, and thorough documentation—organizations can harness the full power of their book of accounts and build a foundation for sustainable growth.

![Comment valider la cohérence BALANCE - GRAND-LIVRE en une minute [pour Auditeur]](https://i.ytimg.com/vi/5mEa8UvnGTg/mqdefault.jpg)